.svg "logo (1)")

Read time: 5 minutes

Small businesses drive local economies, but too many still struggle to access timely, right-sized credit. For financial institutions, this is no longer just a demand issue. It is a structural mismatch between how small businesses need financing and how banks underwrite it.

That mismatch is widening the credit gap. Increasingly, AI-driven underwriting is the most practical way to close it.

A Market Defined by Defensive Demand

Small business credit demand remains strong, but the nature of that demand has shifted. Businesses are not just borrowing to grow, they are borrowing to manage rising costs, uneven cash flow, and economic uncertainty.

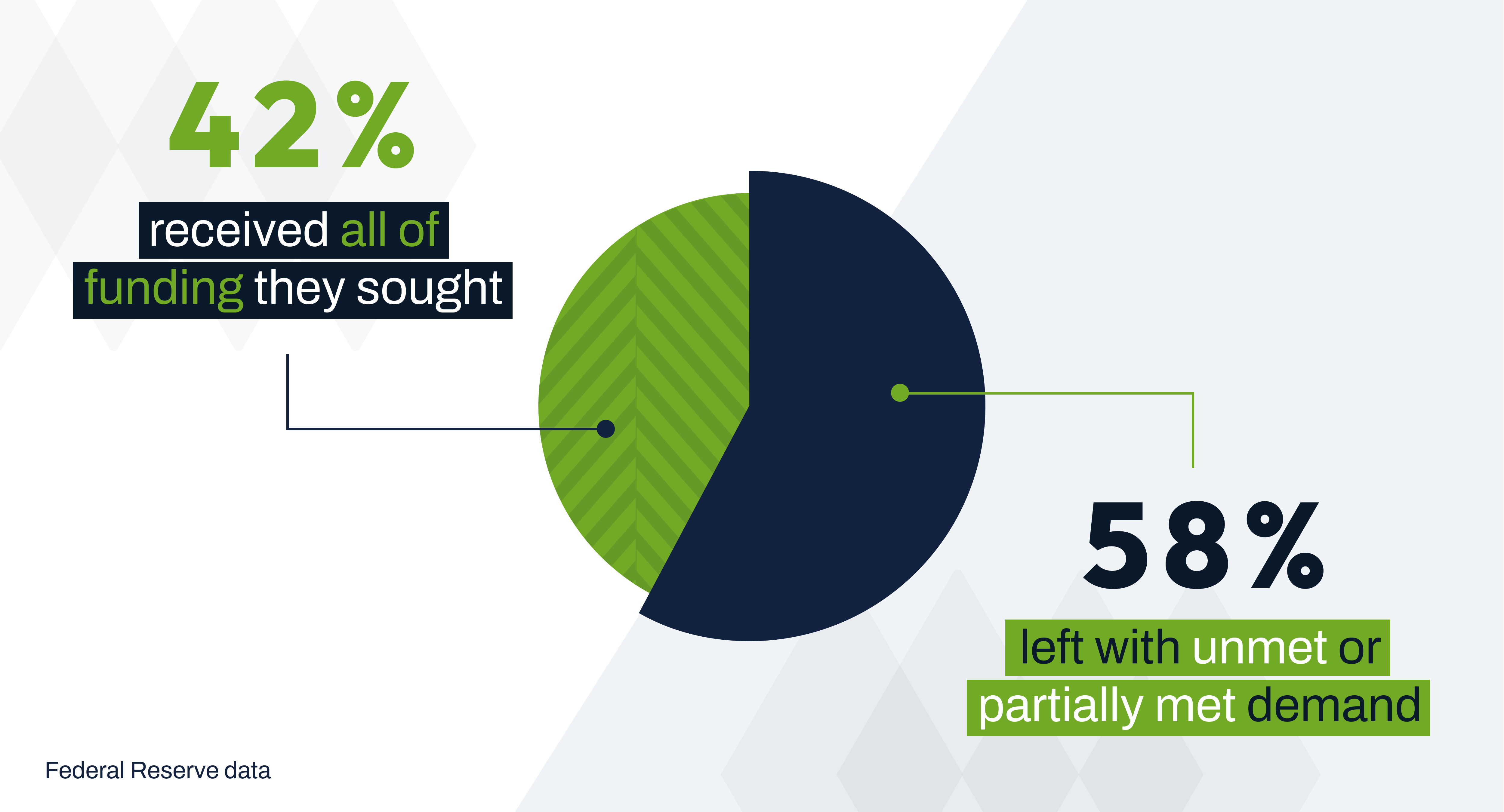

Federal Reserve data shows that 60% of employer firms applied for financing, yet only 42% received all the funding they sought, leaving 58% with unmet or partially met demand¹. Operating expenses, not expansion, are the most common reason for borrowing¹.

Traditional underwriting was built for expansion lending. It relies heavily on historical financials, tax returns, and static ratios. In today’s environment, those tools often miss what matters most: current cash flow.

The result is a growing disconnect. A rising share of denied applicants cite excessive existing debt, 41% in 2024, up from 22% in 2021, even as many businesses face temporary cash-flow strain rather than structural decline¹. Lenders can see stress. They cannot always see whether it is temporary or structural. That is the core problem.

Why Traditional Underwriting Breaks Down

The limitations of legacy underwriting are most visible in small-balance lending.

- Outdated data. Financial statements and tax returns can lag real conditions by six to eighteen months, while smaller businesses often lack robust credit histories².

- Manual processes. A $50,000 loan often requires the same steps as a much larger loan, driving high costs and long cycle times².

- Inconsistent decisions. Human-driven workflows introduce variability, making it harder to apply policy consistently and manage fair-lending risk.

- Limited insight. Traditional methods struggle to evaluate borrowers in the “messy middle,” those who do not meet standard criteria but may still be viable.

These challenges make small loans difficult to justify economically. As a result, many banks either avoid them or process them inefficiently.

The Small-Loan Opportunity Banks Can’t Ignore

Demand is shifting toward smaller credits. SBA data shows that loans under $150,000 have doubled since 2020 and continue to grow, while Federal Reserve data indicates that 40% of applicants seek less than $50,000³¹. Historically, banks have underserved this segment because the economics did not work. Manual underwriting made small loans nearly as expensive to originate as larger ones².

Fintechs stepped in, offering faster decisions and simpler experiences. Borrowers followed, even when costs were higher. For banks, the trade off is clear: continue to lose share or find a way to serve this segment profitably.

How AI Enabled Underwriting Changes the Math

AI enabled underwriting improves both speed and decision quality by using real-time data and automation.

- Real-time cash-flow insight. Transaction data provides a current view of revenue, expenses, and liquidity, far more timely than traditional financial documents².

- Sharper risk segmentation. Data-driven models help distinguish temporary strain from structural risk, improving approval accuracy in a more complex borrower environment².

- Faster decisions. Traditional SME lending can take weeks to approve and months to fund, while digital models can deliver decisions in minutes and funding within 24 hours⁴.

- Lower costs. Automation reduces manual effort per application, making small-balance lending economically viable².

- Consistent, explainable outcomes. AI systems apply policy uniformly and support clear adverse-action reasoning, aligning with regulatory expectations⁶.

- Ongoing monitoring. The same data used for underwriting can provide early warning signals post-origination, strengthening portfolio oversight².

This is the real unlock: better decisions at a lower cost per loan.

Why Acting Now Matters

The urgency is growing across three fronts.

- Borrower expectations. Small businesses expect fast, digital experiences and are willing to look beyond banks to get them.

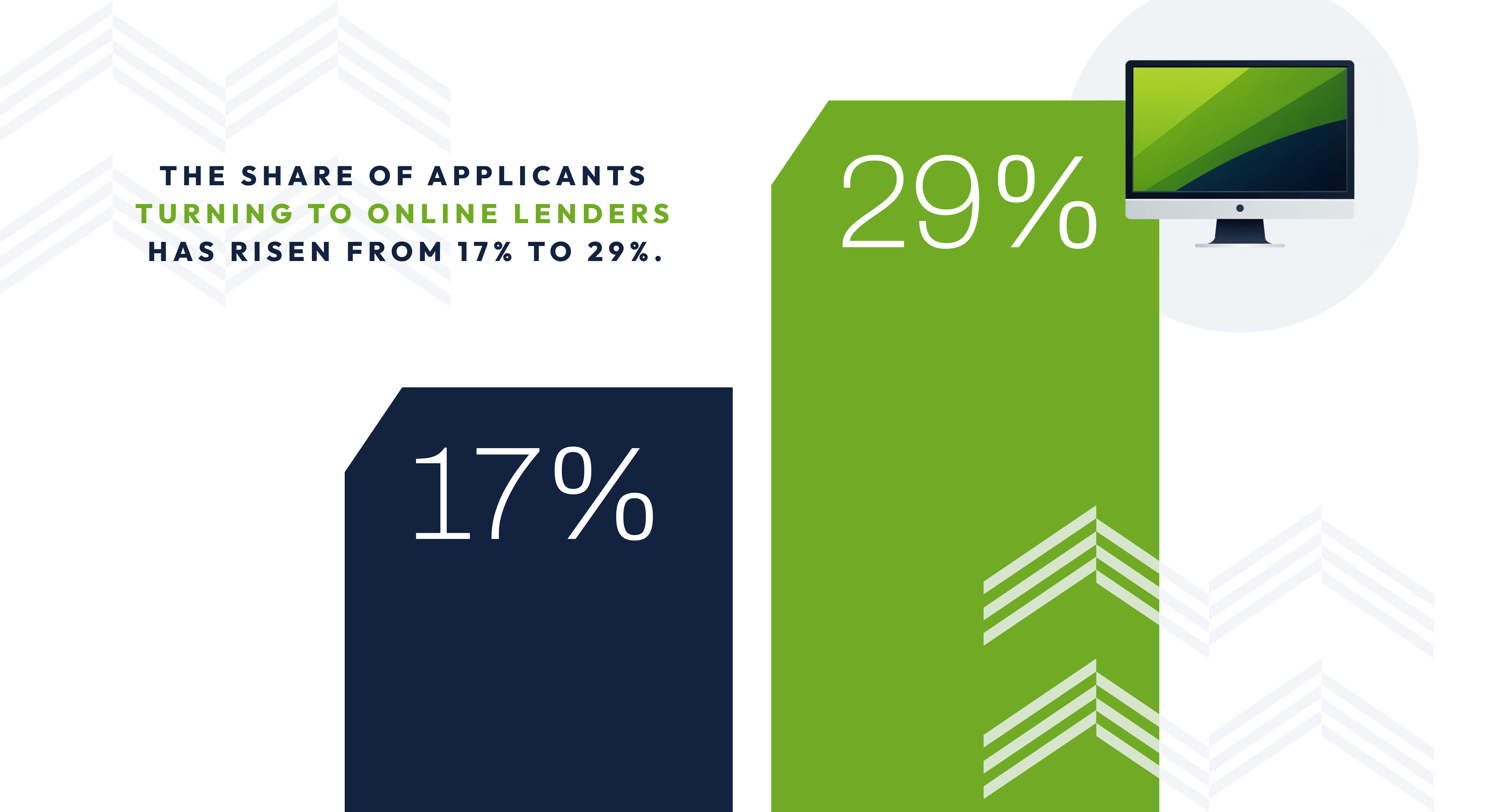

- Competitive pressure. The share of applicants turning to online lenders has risen from 17% to 29%, even though many report higher-than-expected costs¹.

- Rising complexity. Cost pressures, uneven cash flow, and higher debt levels make borrowers harder to evaluate using static data alone¹.

Without change, banks face a losing equation: decline small loans and lose relationships or book them at high cost.

Responsible AI Is the Differentiator

AI enabled underwriting must meet the same standards as any credit process: transparency, fairness, and control. Regulators require explainable decisions, accurate adverse-action reasons, and active fair-lending oversight. There is no exemption for AI-driven models⁶.

The most effective approach combines automation with human oversight: automate straightforward approvals and declines, route complex cases to underwriters, and monitor outcomes and model performance⁵. This ensures speed without sacrificing governance.

Turning Strategy into Execution

Closing the credit gap starts with focus: target existing small business customers, prioritize loans between $25,000 and $250,000, use cash-flow data as the foundation, and build hybrid workflows that combine automation and human review.

From there, institutions can scale, expanding to new customers and integrating lending into broader relationship strategies.

How Baker Hill Helps

Many institutions recognize the need to modernize underwriting but face execution challenges. Baker Hill enables this transition with integrated loan origination and underwriting workflows, AI-driven cash-flow analysis, automated data ingestion, configurable credit policies, and explainable decisioning. These capabilities help institutions improve speed, consistency, and cost efficiency while maintaining strong governance.

Small business lending is becoming a technology-enabled relationship business. Speed, data, and precision now define competitiveness. Banks that modernize can turn small-balance lending into a scalable growth engine. Those that do not risk losing both market share and customer relationships. The opportunity is clear, and time sensitive.

To learn how your institution can close the small business credit gap with AI underwriting, explore Baker Hill’s solutions or request a demo today.

___________________________________________________________________________________________________________________

Sources

- Federal Reserve, 2026 Small Business Credit Survey; financing demand, approval rates, borrower challenges, and online lender usage trends.

- FinRegLab, research on cash-flow underwriting, data limitations, and small-business lending economics.

- U.S. Small Business Administration (SBA), FY2024 Capital Report; growth in small-dollar lending under $150,000.

- McKinsey & Company, The Value in Digitally Transforming Credit Risk Management; SME lending cycle times and digital benchmarks.

- Federal Reserve Bank of Kansas City, Q4 2025 Small Business Lending Survey; credit standards, approval rates, and lender behavior.

- Consumer Financial Protection Bureau (CFPB), Department of Justice (DOJ), Federal Trade Commission (FTC), Equal Employment Opportunity Commission (EEOC); guidance on AI, explainability, and fair lending compliance.

__________________________________________________________________________________________________________________________